Accrued (or Unbilled) Revenue

What Is Accrued or Unbilled Revenue?

Accrued revenue is revenue that a company has earned but hasn’t received, typically because the customer hasn’t been invoiced yet or still has to pay. In accounting, especially in line with Generally Accepted Accounting Principles (GAAP) and the International Financial Reporting Standards (IFRS), you’re required to record expenses and income when they are earned, not necessarily when you’re paid.

Accrued revenue is particularly important for service businesses, which typically collect a portion of payment after services are delivered. It’s also important for SaaS companies, as income often comes from monthly, bi-annual, or annual subscriptions. Tracking accrued revenue gives you a real-time view of the company’s financial health by tracking your income as it’s earned, even before the money lands in your bank.

Categories

Table of Contents

Accrued Revenue vs. Deferred Revenue

Accrued revenue shouldn’t be confused with deferred revenue or unearned revenue. While related, these two metrics are distinct and serve different purposes. Essentially, both metrics are influenced by Generally Accepted Accounting Principles (GAAP), which state that revenue is recognized when services are delivered, not when payment is made.

| Accrued Revenue | Deferred Revenue | |

|---|---|---|

| Meaning | Revenue that a company has earned but hasn't yet received. | Money received by a company for services or products yet to be delivered. |

| Revenue Recognition | Revenue is recognized when services are provided, even if payment hasn’t been received. | Revenue is only recognized as the service is delivered over time, even if the entire payment is received upfront. |

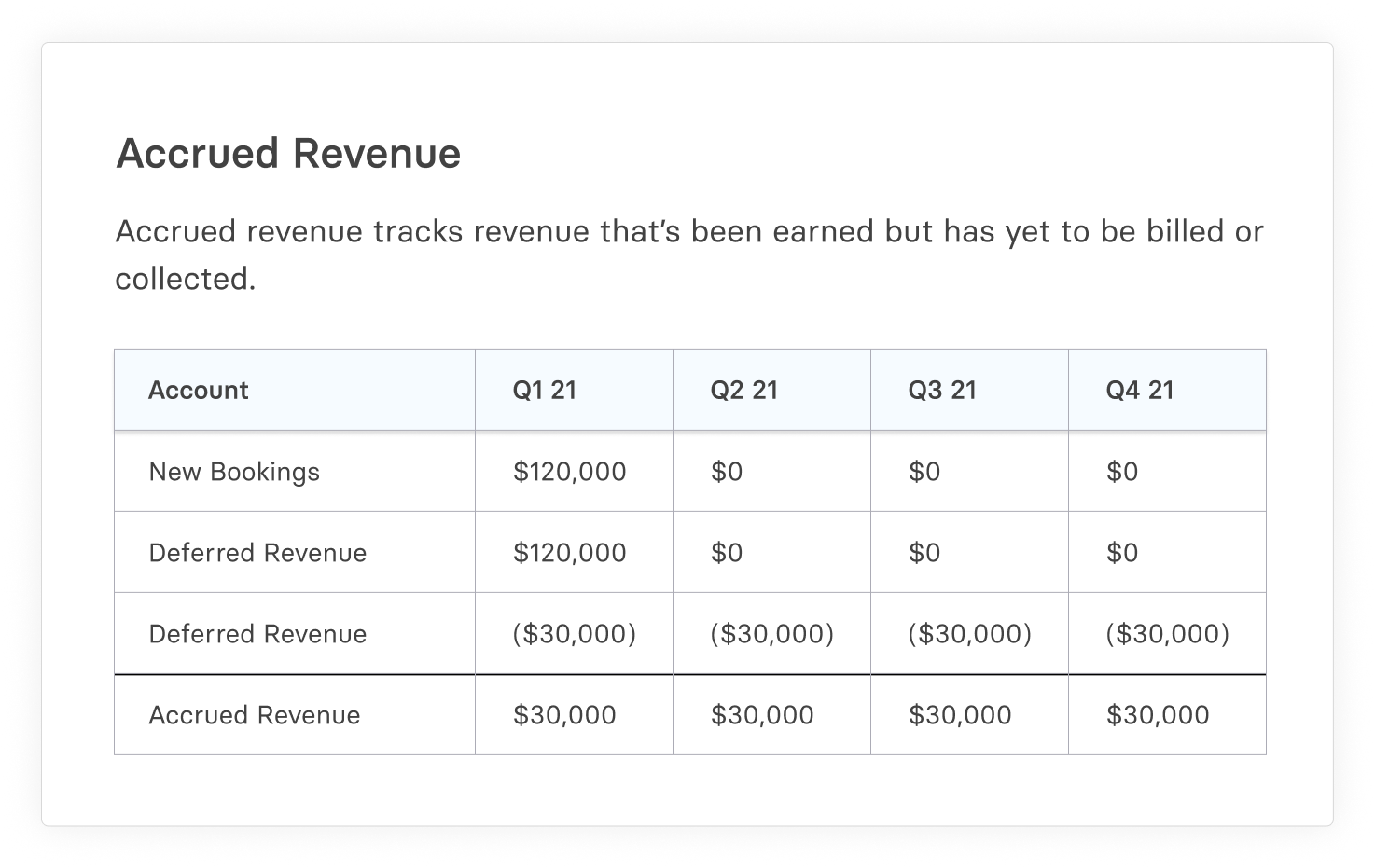

| Example | A SaaS company earns $100 in January for a service provided but hasn't billed the customer or received payment yet. This $100 is accrued revenue for the month. | A customer pays $1,200 for a yearly subscription in January, but the company delivers the service monthly. So, in January, only $100 is earned, and $1,100 is deferred revenue. As services are provided monthly, $100 moves from deferred to earned. |

| Impact on Financial Statement | Increases revenue on the income statement before cash is received. | Increases liability on the balance sheet (as unearned revenue) until the service is provided. |

| Importance in SaaS | It gives a real-time view of earned revenue and the company's operational efficiency. | Reflects the company’s financial obligations to deliver services at a later date. |

Let’s start with accrued revenue. Simply put, accrued revenue is income or revenue your company has earned but hasn’t yet received, likely because you haven’t billed your customer or the customer hasn’t made the payment yet. SaaS companies often run on a subscription-based business model, so accrued revenue is a critical metric in SaaS accounting.

Accrued revenue helps you understand how much income you’ve truly earned in a month and gives you real-time insights into your company’s operational efficiency and financial health. By matching revenue earned with the services provided within the same period, regardless of when the payment is received, you’ll have a clearer picture of your company’s immediate financial performance.

In contrast, deferred revenue refers to money not earned yet, meaning customers have paid you even though you haven’t (completely) provided the services. In SaaS, customers often sign up for subscriptions on a monthly, quarterly, bi-annual, or yearly basis, so even if your company collects the money upfront for the entire duration of the subscription contract, you’ll only consider the portion for which services have already been provided as earned revenue, and the rest is deferred.

Examples of Accrued or Unbilled Revenue in Real-World Scenarios

To understand accrued revenue better, let’s look at hypothetical accrued revenue examples.

Say Company A provides advertising services and charges clients based on the number of ad impressions delivered. Clients are billed monthly at the start of the following month.

Throughout January, Company A delivers 2 million ad impressions for a client, priced at $5 per thousand impressions. At the end of the month, the company has $10,000 of accrued revenue (2 million impressions / 1,000 * $5) for the service provided in January — even though the customer will only be invoiced and payment will be processed the next month.

Let’s consider another example. Company B is working on a project that is expected to last several months. According to the contract, the company will invoice the client based on milestones achieved, regardless of the time spent working on the project.

Company B completes work valued at $15,000 before the end of January, but can only bill the client in early February when it reaches the next milestone. Despite not billing the client in January, Company B recognizes $15,000 in accrued revenue for January’s work on the company’s balance sheet, acknowledging the value of the service provided in that accounting period.

In both cases, there’s a small window between when the services are delivered, the customer is billed, and when payment is received. During this time, the income is considered accrued and eventually adjusted in the income statement once revenue has been received.

How to Calculate and Record Accrued (Unbilled) Revenue

Calculating accrued revenue is simple. Add up the amount of revenue from all customers who have received services in a particular period but have not yet been billed. This total is your accrued revenue for the period.

However, when you calculate or log accrued revenue, keep these considerations in mind:

- SaaS contracts might span several months or years. So, you must consistently and carefully track and recognize the revenue to match the earnings with when the service is delivered.

- If a free trial leads to a paid subscription without interruption, you should recognize the transition in your accounting books to reflect when the paid service period begins accurately.

Below, we’ve shared a brief guide to help you understand how to record accrued revenue in your accounting books in line with GAAP’s matching principle.

Guidelines for Accrued Revenue Journal Entries

In the accrual accounting method, accurate journal entries for accrued revenue are essential to reflect the company’s financial position truthfully. By recording revenue in the correct periods according to GAAP’s revenue recognition principle, you ensure that your stakeholders receive a clear and reliable view of your financial performance.

That said, recording accrued revenue is pretty straightforward if you’re familiar with double-entry bookkeeping and basic accounting concepts such as trial balance, balance sheets, or accrued income statements.

At a high level, there are two main steps involved in recording accrual revenue:

- Recording accrued revenue when you earn or accrue revenue before receiving payment.

- Adjusting revenue entries after invoicing and receipt of payment to reflect the transition from accrued revenue to accounts receivable and then to cash.

When recording an accrued revenue journal entry, each transaction will be reflected as “earned revenue” on the income statement and as a “current asset” on the balance sheet. Typically, you will debit an accrued revenue account and credit a revenue account. This entry increases your company’s assets because it represents money that you expect to receive. It also improves your revenue, showing the earnings for that period.

Once a customer has been invoiced but payment hasn’t been received, you can turn the accrued revenue into “accounts receivable.” When you finally get the payment, you can convert the “accounts receivable” to cash, so record an adjusting entry in the revenue account — this will change the balance sheet but won’t touch the income statement.

The Role of Accrued Revenue in Financial Analysis

As we’ve established, accurate management of accrued revenue is essential to produce reliable financial statements — a fundamental need for finance teams, as data underpins all strategic financial decisions.

By tracking accrued revenue, you can better understand your company’s cash flow situation, assess its financial health with revenue forecasting, and make informed decisions about future investments or expenses. Plus, aligning revenue recognition with service delivery gives you a more precise measure of the company’s profitability and operational efficiency.

Most importantly, accrued revenue is essential for maintaining transparency with stakeholders, demonstrating your company’s growth potential, and complying with accounting standards (check out our page on cash accounting vs accrual accounting for more information). All this to say, it’s a key component of financial analysis and strategic planning.

Navigating Accrued Revenue Challenges in SaaS

Managing accrued revenue comes with unique challenges, and the SaaS industry adds another layer of complexity. Here’s how:

- SaaS models typically involve subscriptions, which complicates revenue recognition. So, it can be difficult to accurately track and report on revenue according to accounting standards. A comprehensive, robust FP&A software like Mosaic can make all the difference.

- If you rely on manual processes to track accrued revenue — or any other financial metrics — you’ll likely see errors and inconsistencies, which is the last thing you need, considering the significant time invested in the process. Luckily, Mosaic’s Metric Builder simplifies the metric calculation and tracking for SaaS finance teams.

- Understanding the timing of cash inflows from accrued revenue is crucial to effectively managing cash flow. Still, in reality, this can be challenging, considering the nature of SaaS billing cycles.

- Compliance and reporting can throw you a curveball if you’re not prepared. Specifically, it’s essential to keep up with evolving accounting standards and ensure compliance by accurately reporting financial performance.

Mosaic is a strategic finance platform designed specifically for SaaS — it can be invaluable when understanding your accrued revenue. With Mosaic, SaaS companies can tackle the challenges of tracking accrued revenue, streamline their processes, and boost financial accuracy and compliance — all through a single platform.

Best Practices for Managing Accrued Revenue

There are a few things you can do to get the best view of your accrued revenue and manage it well. Below, we’ve shared some tips to get you started:

- Work with solid software, especially one that suits the SaaS and professional services business models. You need one that can automate the process of recording accrued revenue, reduce errors, and save time — Mosaic can help you here.

- Regularly reconcile accrued revenue accounts with actual receipts. This enables you to quickly identify discrepancies between recorded revenues and cash received and ensure the financial statements accurately reflect the company’s position.

- Frequently analyze accrued revenue to understand patterns or trends that can offer insights into business performance and help you make informed strategic decisions.

- Regularly review your financial statements to ensure accrued revenue is properly recorded and recognized.

In the end, an efficient, reliable financial planning and analysis process (FP&A) is at the heart of effectively managing accrued revenue and other metrics and setting a solid foundation for your company’s growth.

Accrued / Unbilled Revenue FAQs

What is the difference between accounts receivable and accrued revenue?

Accrued revenue represents earned income for services or products yet to be billed to the customer, while accounts receivable are funds owed to a company for services or products already invoiced but not yet paid for. Essentially, the difference lies in whether an invoice has been issued to the customer.

How does accrued revenue impact cash flow?

Can accrued revenue be considered an asset?

What is unbilled revenue?

Explore Related Metrics

Own the of your business.