Average Collection Period

What is the Average Collection Period?

Average collection period refers to how long it typically takes to collect payment from your customers after you’ve delivered a product or services, i.e., accounts receivables. In other words, it’s the average period of time between the “sale” or completion of services and when customers make payment for a given period.

Categories

Table of Contents

Impact Of Average Collection Period On Your Bottom Line

The average collection period is mostly relevant for credit sales, as cash sales receive payments right when goods are delivered. That’s why this metric impacts professional service companies more than others, where payments are typically staggered based on when and how services are completed.

Regardless of your company’s industry, tracking the average collection period is essential. Here’s why: It gives you insight into your organization’s credit policies and allows you to spot potential cash flow crunches before they happen.

Typically, a more extended average collection period puts pressure on your company’s cash flow because your money is tied up in receivables, making it harder for you to pay your vendors, employees or reinvest in the business. A more extended average collection period also increases the chances of growing customer debt or accounts receivable (AR) going unpaid. Plus, the impact is greater for professional service companies, as you don’t have physical assets or products to fall back on to recuperate those losses.

By proactively monitoring this metric, you can quickly address gaps in your credit or collection policies, ensure your business has enough cash for its operations, and improve billing processes to avoid payment delays and unnecessary administrative costs.

How to Calculate Your Average Collection Period

Average collection period, sometimes referred to as days sales outstanding, is the average time that elapses between your company’s completion of services and the collection of payment from your customers.

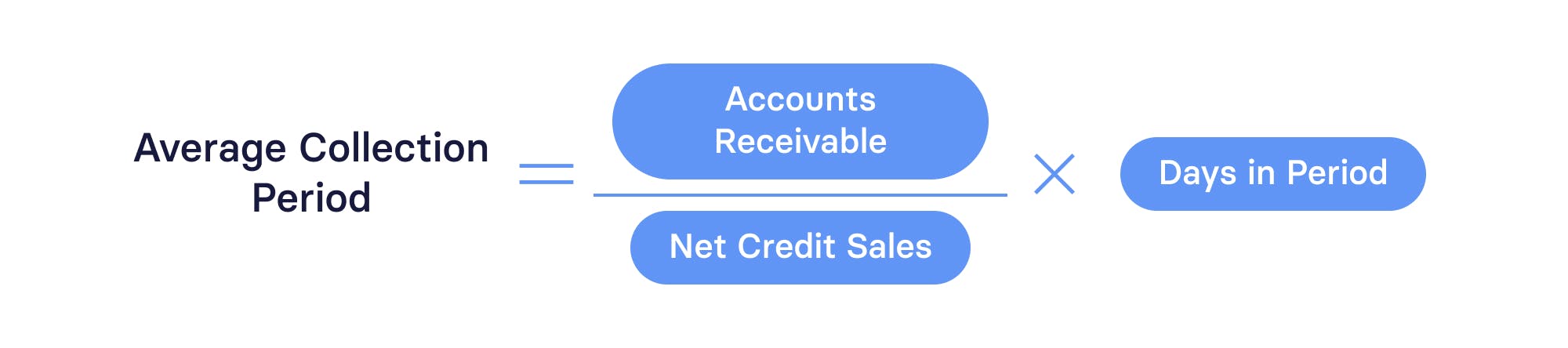

To calculate this metric, you simply have to divide the total accounts receivable by the net credit sales and multiply that number by the number of days in that period — typically, this is 365 days. That said, whatever timeframe you choose for your calculation, make sure the period is consistent for both the average collection period and your net credit sales, or the numbers will be off.

Here’s a straightforward average collection period formula:

If you’d like to calculate your company’s average collection period quickly, feel free to use the calculator below:

Average Collection Period Calculator

Your Average Collection Period

0

Another common way to calculate the average collection period is by dividing the number of days by the accounts receivable turnover ratio.

Example of Average Collection Period Calculation

For instance, let’s say your company offers management consulting services. In 2024, your company reported net credit sales of $2 million; on December 31st, the accounts receivable balance was $500,000. Here’s how you’d find the average collection period:

Average Collection Period for 2024 = ($500,000 / $2,000,000 ) X 365 = 91.25 days

This means that, on average, it takes your company 91.25 days to collect payments from clients once services have been completed.

Benchmarks for Average Collection Period

What do industry benchmarks for the average collection period look like? It depends.

According to the Bank for Canadian Entrepreneurs (BDC), most businesses should have an average collection period of less than 60 days. However, the ideal number depends on the nature of your business, client relationships, and invoice period.

Industries such as banking (specifically, lending) and real estate construction usually aim for a shorter average collection period as their cash flow relies heavily on accounts receivables. On the other end of the spectrum, businesses that offer scientific R&D services can have an average collection period of around 70 days.

Generally, the lower the collection period, the better for business. This means your company’s locking up less of its funds in accounts receivable, so the money can be used for other purposes. Additionally, a lower number reduces the risk of customer defaults and likely reflects that payments are being made on time, depending on your billing cycle.

The Impact of Economic Trends on Collection Periods

As many professional service businesses are aware, economic trends play a role in your collection period. Seasonal fluctuations impact payment behaviors, which in turn affect your average collection period.

For instance, consumers and businesses often face financial constraints during recessions or economic instability. Consequently, this may delay payments or lead to higher defaults on invoices — resulting in longer average collection periods as companies struggle to collect on outstanding receivables. Law firms, for example, reportedly saw an overall increase of 5% in the average collection cycle in 2023. Similarly, inflation also negatively impacts consumers and businesses, often resulting in longer average collection periods.

That’s why it’s important not to take this metric at face value; be mindful of external factors that influence it. If you analyze a peak or slow month in isolation, your insights will be skewed, and you can’t make sound decisions based on those numbers.

Instead, review your average collection period frequently and over a longer duration, such as a year. This way, you’ll understand what the number means and the “why” behind it.

Get the Professional Services P&L Model Template

Improve Your Average Collection Period

Sometimes, your company’s average collection period might be high. The good news? There are a few things you can do to speed up your professional service company’s collection period:

- Bill upfront for set work before it begins. Any overages can be paid on credit terms in arrears.

- Build in payment due dates at different completion points. Bill clients for 50% of a project at the midway point or schedule incremental payments as different phases are complete to ensure you have enough funds to support operations moving forward — this way you don’t perform 100% of the work without getting paid.

- Improve your invoicing and collections processes to avoid cash flow crunches. To speed up payments, you might need to adjust your payment terms. Consider switching from net 30 to net 15, for example.

- Tighten your credit policies. For instance, reduce leniency on late payments and charge penalties when they occur, or don’t provide services on credit for clients with a history of delayed payments.

- To encourage clients to pay invoices before the due date, offer incentives for early payments, such as a discount on the bill rate for the subsequent services they sign up for.

- Ensure your team follows up more rigorously to ensure timely collections, like sending frequent reminders to avoid delayed payments.

All these efforts will help you maintain a healthy cash flow, sustain business operations effectively, and reduce your risk of bad debt. But most importantly, try to avoid credit sales altogether by billing upfront whenever possible to avoid cash flow issues.

Role of Mosaic in Optimizing Collection Periods

As we’ve said before, the average collection period offers limited insights when analyzed in isolation.

To get the most out of this metric, tailor it to your business needs. This way, you’ll get more nuanced, actionable insights that can fuel business growth. That’s where a strategic finance platform like Mosaic comes in.

Mosaic lets you automate your average collection period calculation and dig into the data using Metric Builder, including (but not limited to) the following ways:

- Analyze collection times by customer segments to focus collection efforts.

- Compare payment collection speeds across different contract lengths, such as three-year versus one-year contracts, to get a thorough view of your company’s financial health. This is particularly important in an industry impacted by seasonal fluctuations.

With Mosaic, you can also get a real-time look into your billings and collections process. Since Mosaic offers an out of the box billings and collections template, you can automatically surface outstanding invoices by due date highlighting exactly where to focus your collection efforts.

With Mosaic you can automatically track your average collection period or days sales outstanding metric to see if your customers are paying according to your benchmarks. This will help your company nail its cash flow targets and ensure you don’t end up in a cash flow crunch.

The average collection period should be used in your financial model to accurately forecast how and when new customers will contribute to your cashflow.

Also, keep in mind that the average collection period only tells part of the story. To really understand your accounts receivables, you need to look at this metric in tandem with related metrics like AR turnover, AR aging, days payable outstanding (DPO), and more. And that’s just a glimpse of what Mosaic has to offer.

To see Mosaic’s firepower firsthand, request a demo.

Average Collection Period FAQs

Is a shorter average collection period always better?

In most cases, a lower average collection period is generally better for business as it indicates faster cash turnover, which improves liquidity and reduces credit risk. However, if the shorter collection period is due to overly aggressive collection practices, it runs the risk of straining customer relationships, potentially leading to lost business.

How often should companies review their average collection period?

What factors affect the average collection period?

Explore Related Metrics

Own the of your business.